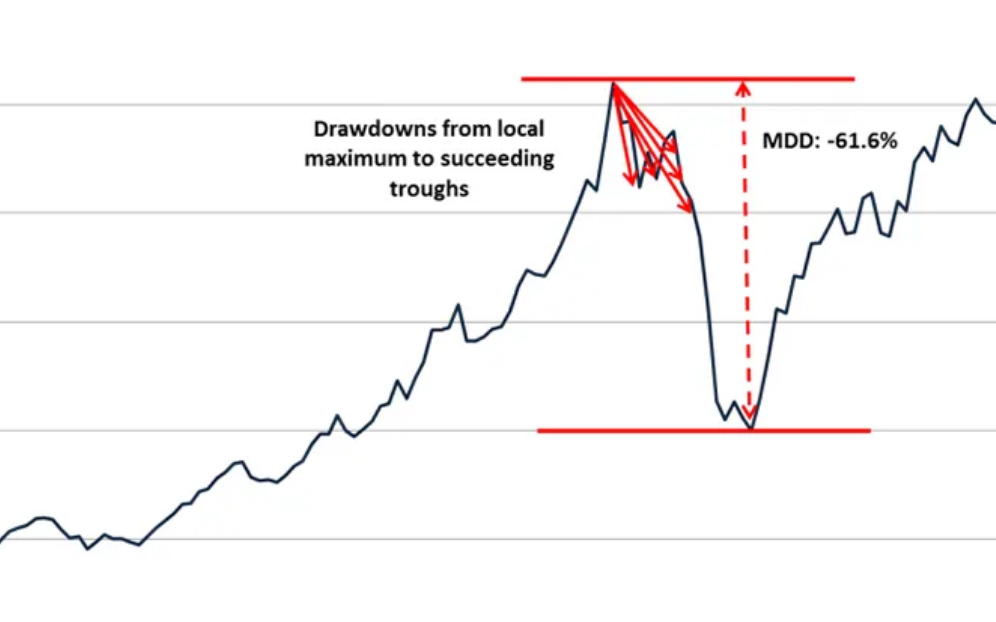

The maximum drawdown (MDD) is the max loss from a peak to trough of the portfolio, before a new peak is attained. It includes both Realized Profit / Loss and Unrealized Profit / Loss. Maximum drawdown is an indicator of downside risk over a specified time period.

The formula for maximum drawdown is:

MDD = (Trough Value – Peak Value) / Peak Value