In this lesson you will learn how to create and backtest trading strategies to buy call options when a stock hits oversold conditions.

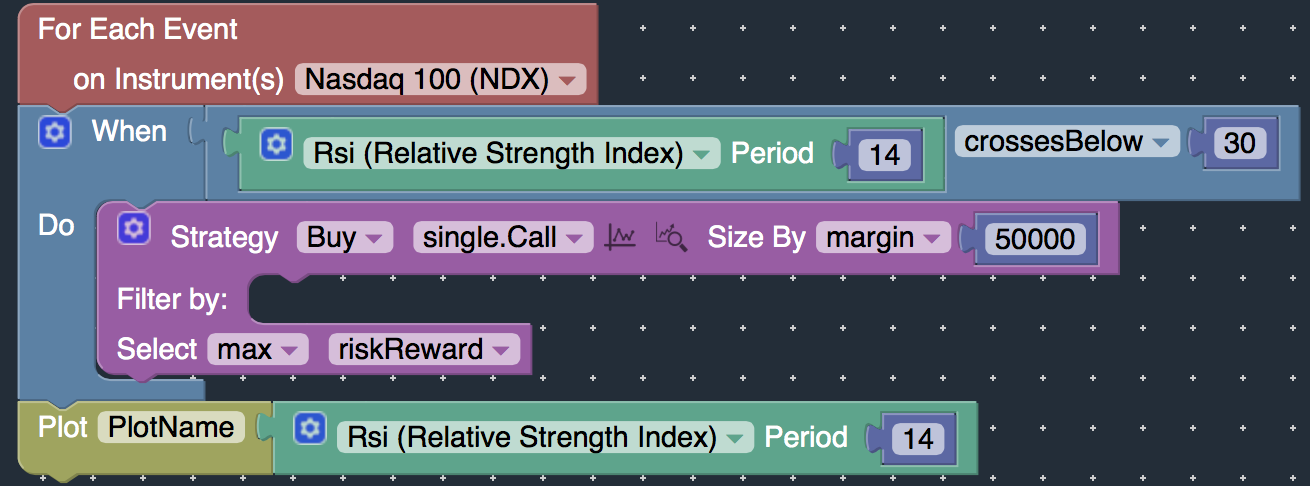

We will construct an options trading strategy that will purchase call options when the underlying stock is considered oversold by the RSI indicator.

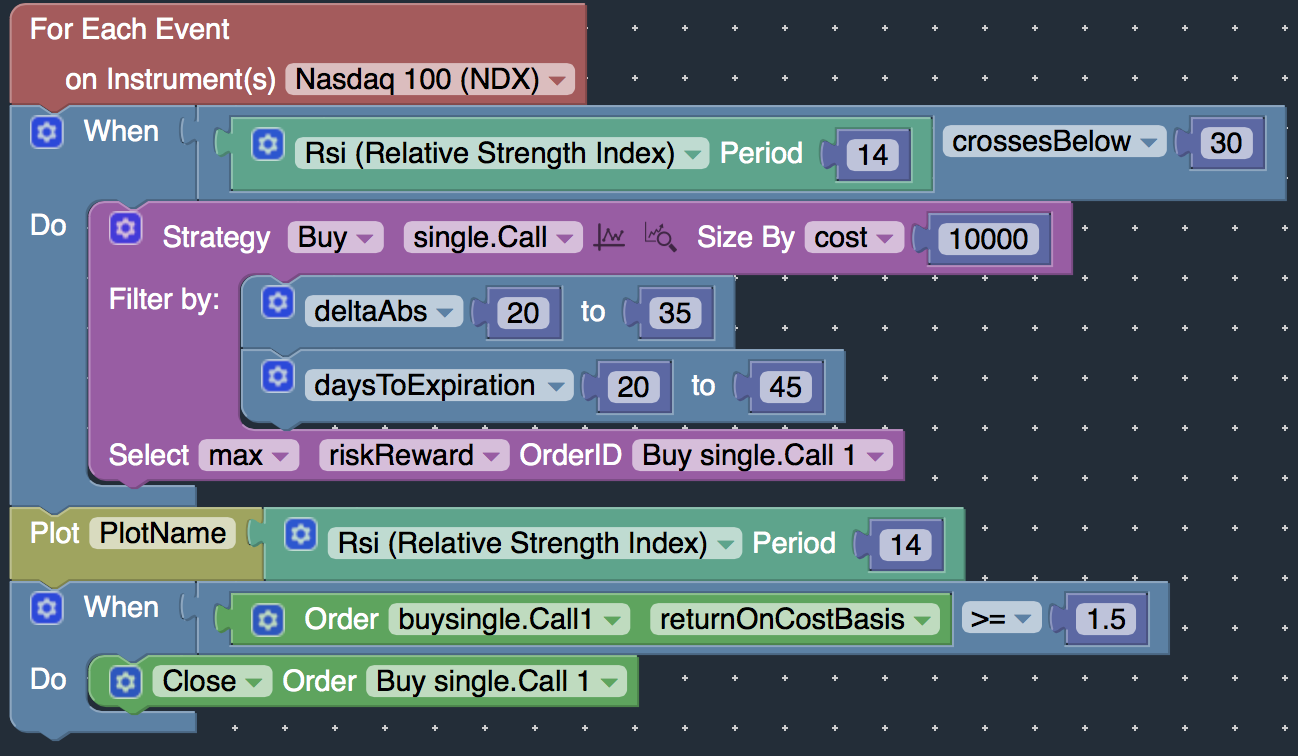

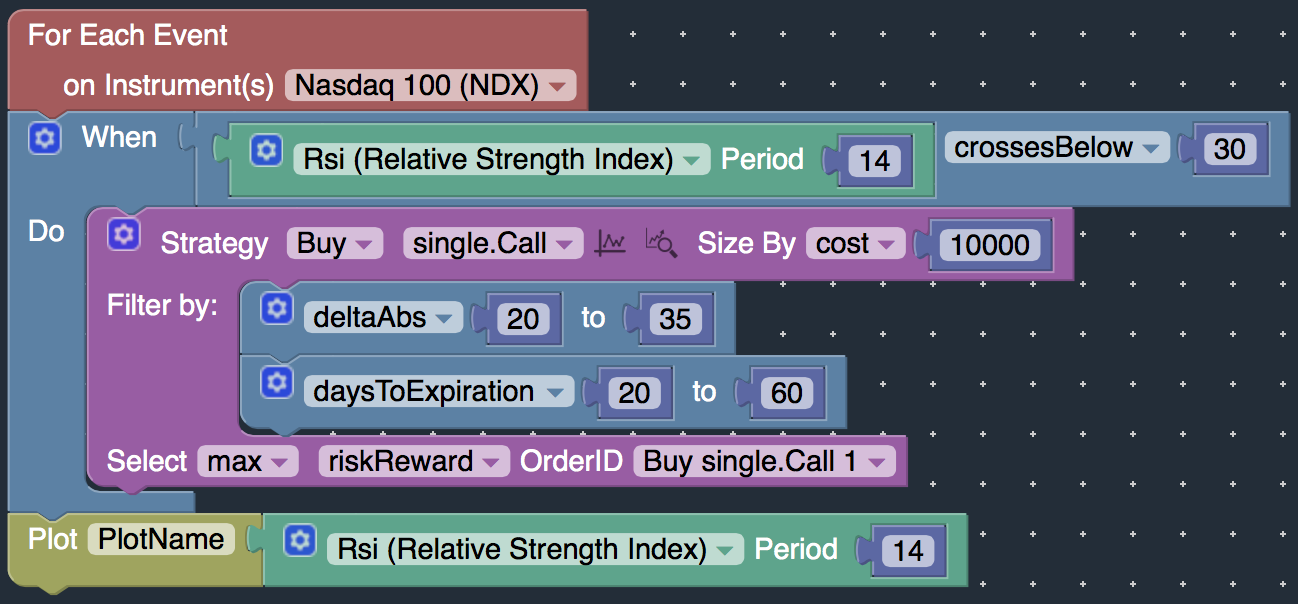

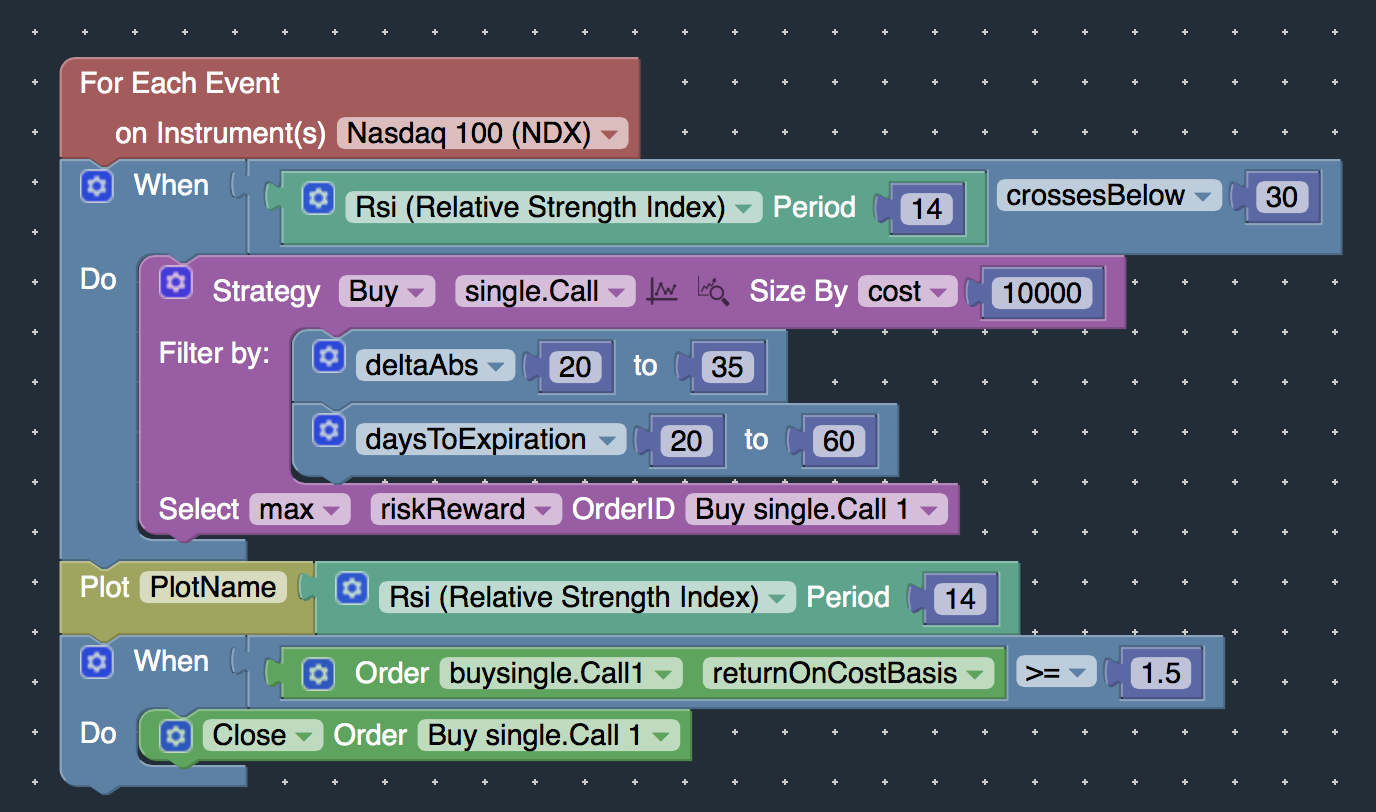

Specifically, we will buy call options whenever the RSI indicator crosses below 30, which is considered an oversold condition. And then we will close the trades when the trades makes 150% or greater return on investment.

Simply click the “Run Backtest” button below to automatically get started.

Call Option

A call option is an agreement that gives an investor the right (but not the obligation) to buy a stock, bond, commodity, or other instrument at a specified price within a specified time frame.

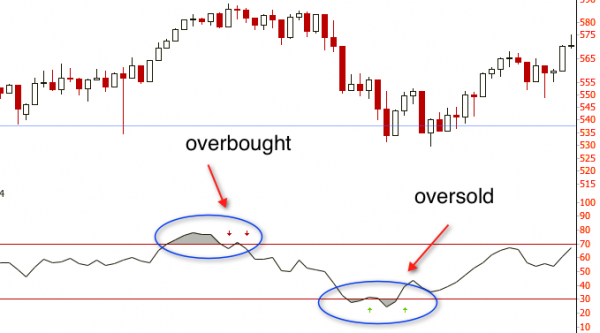

Oversold Indicators

One of the most common indicators of overbought or oversold conditions is the Relative Strength Index (RSI) indicator.

- In this example, we will create a strategy to:

- Buy out-of-the-money call options when the RSI crosses below 30 (an oversold condition).

- Close the call options when the profit exceeds 150%.

- First, login to the OptionStack platform. Select “New Strategy” from the “File” menu item

- Enter any arbitrary name you would like for the strategy

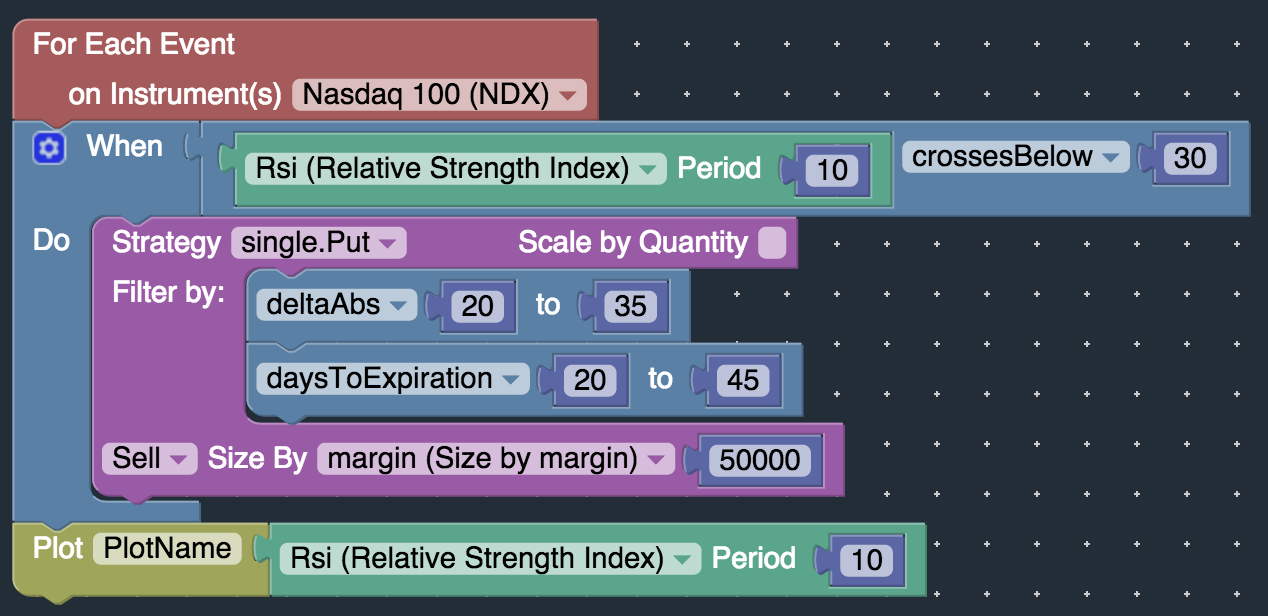

A visual strategy template will be automatically created for you. You can modify this template to define your trading rules.

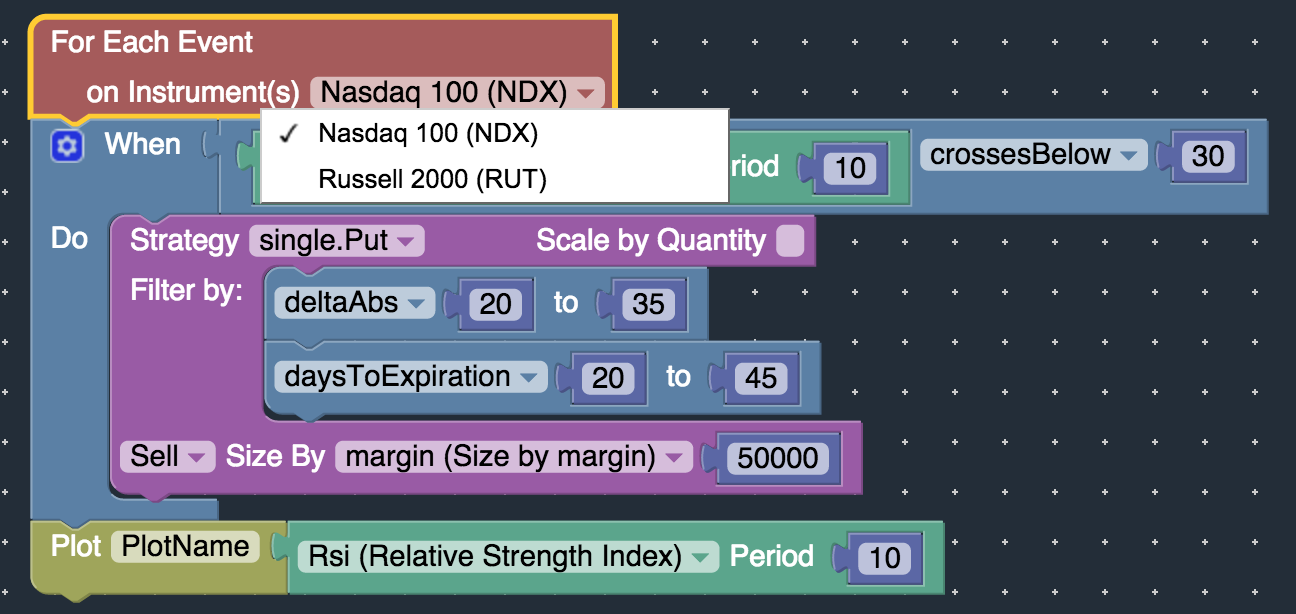

- Define which stock you would like to trade. In this example, we will use the NDX (Nasdaq 100).

- We can plot the RSI to visualize the entry / exit points.

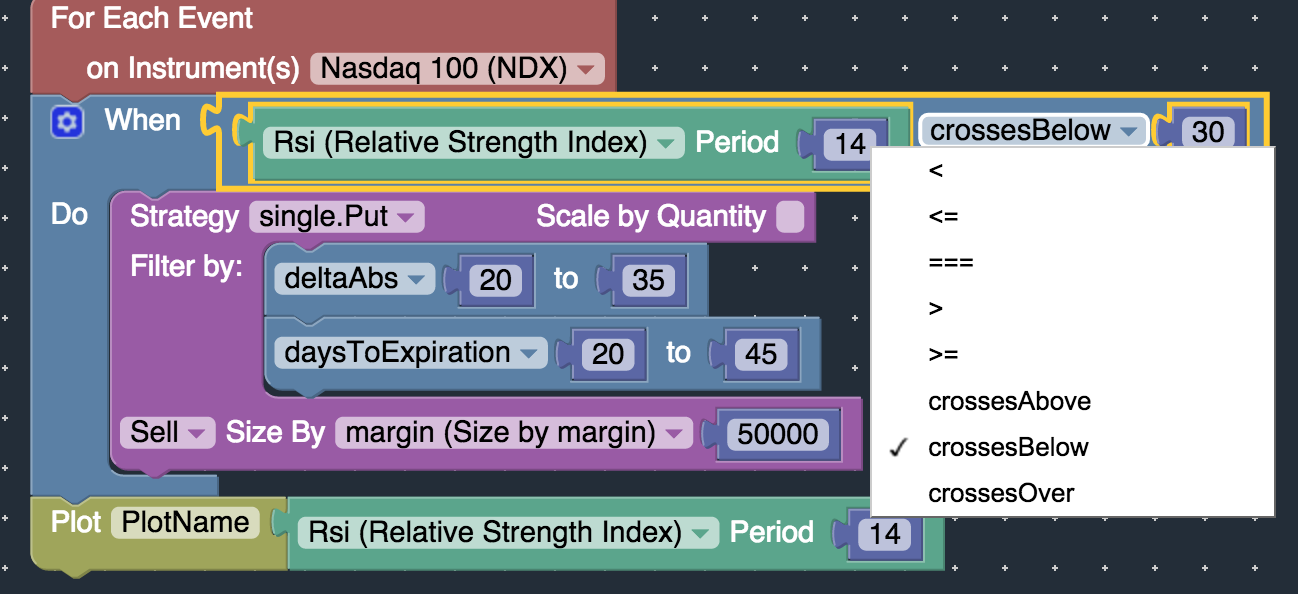

- Define a rule to check when the Relative Strength Indicator (RSI) crosses below 30.

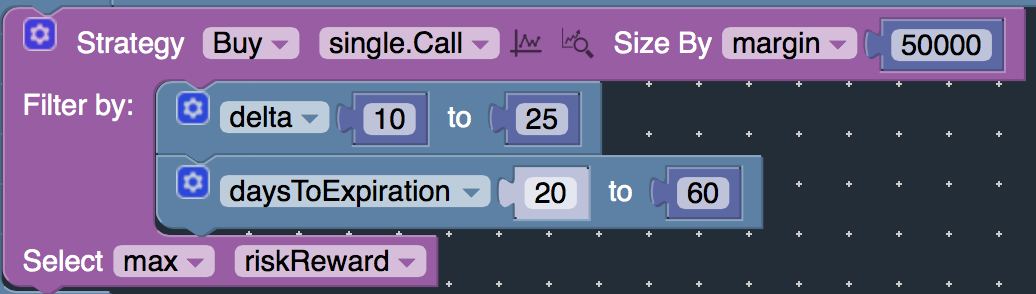

- Define which call option to buy using the Visual Option Spread Builder tool.

- In this example, we will first look for out-of-the-money calls with Delta between 10 – 25 and Days To Expiration between 20 – 60 days.

- Determine how many call options to buy.

- There are several options to calculating the position sizing, such as quantity, cost, margin, risk, delta, etc.

- In this example, we will size based on cost, where we will purchase a quantity equal to about $10,000 in cost.

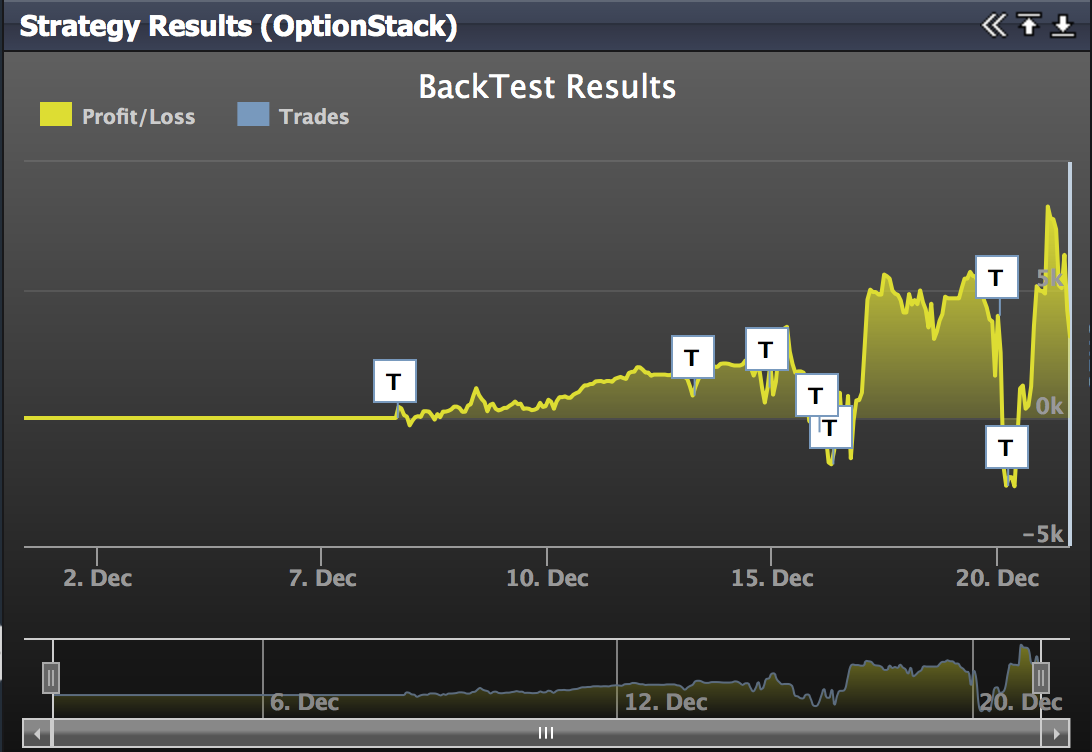

- Now that we have defined our model, we are ready to conduct our backtest.

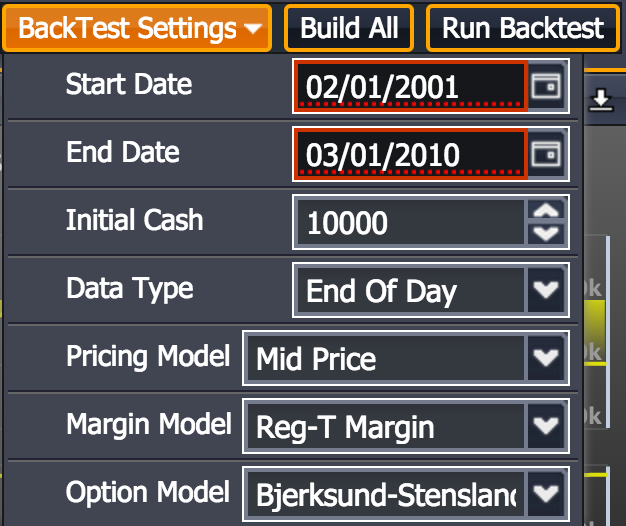

- Before we run the backtest, first review the Backtest Settings.

- Once you have reviewed the backtest settings, click “Run Backtest”

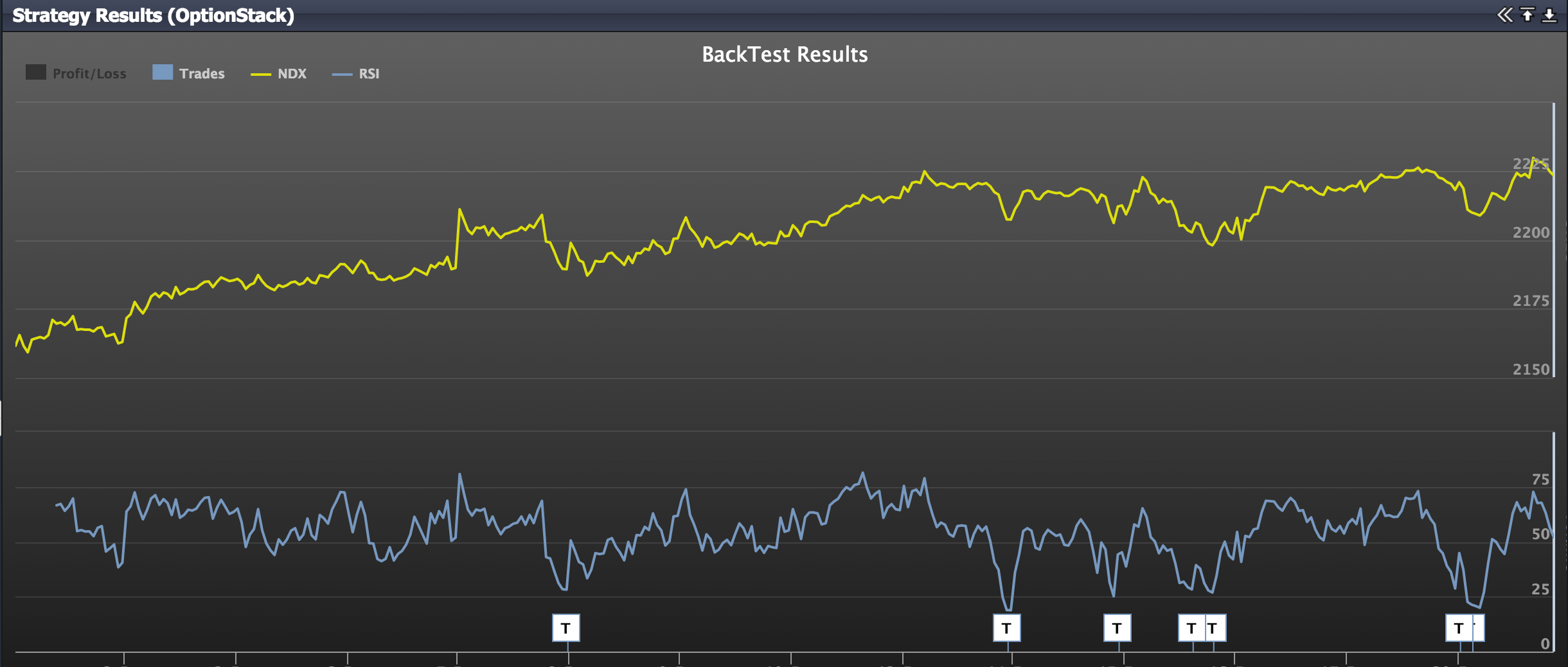

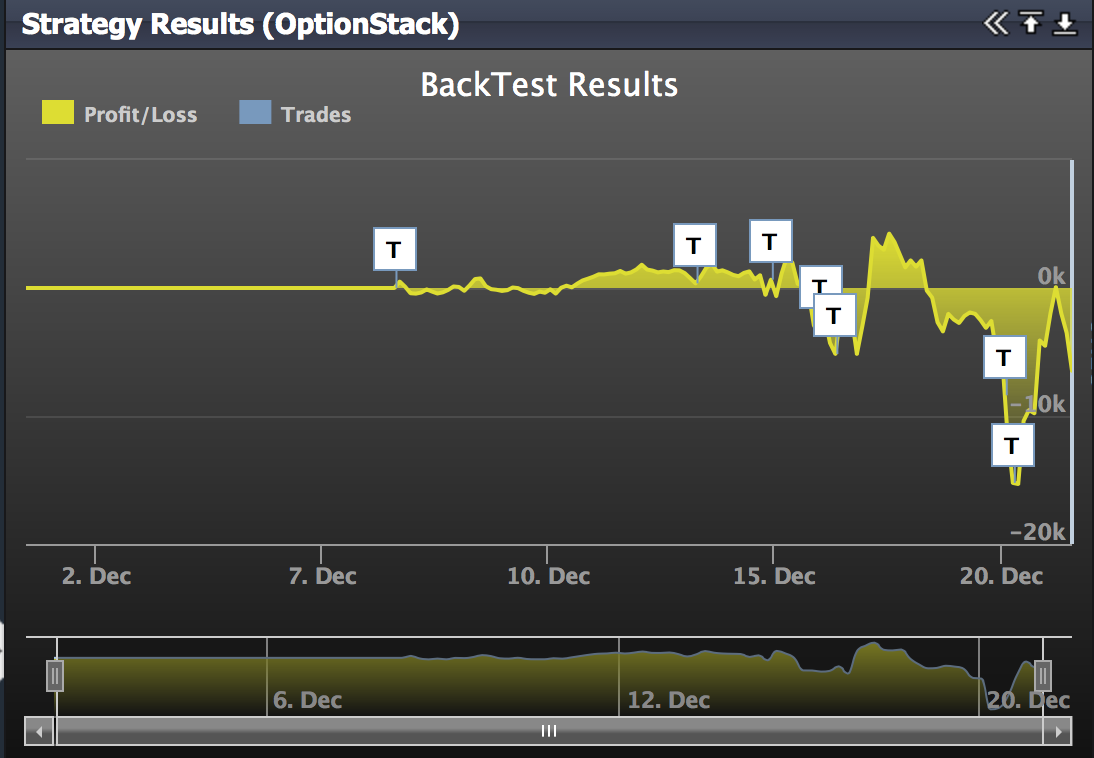

- Once you click “Run BackTest”, the OptionStack platform will automatically evaluate your strategy and provide you with the performance results.

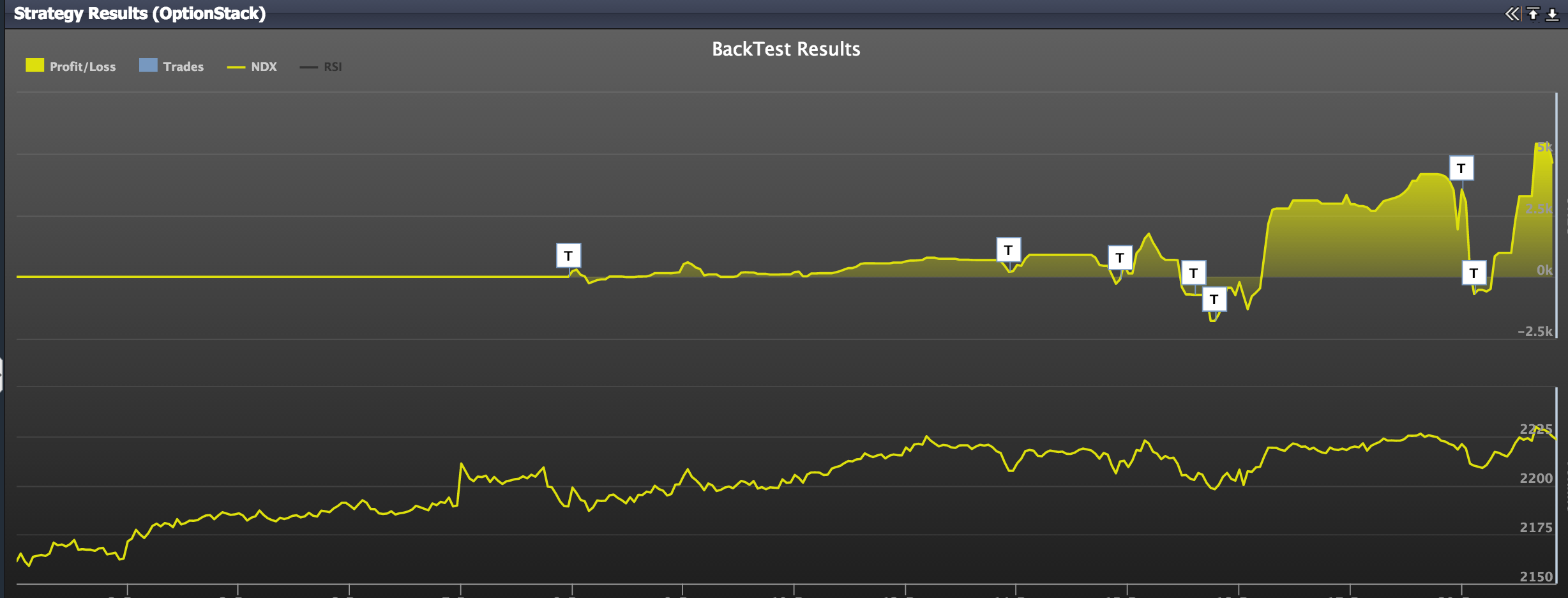

- Now, let’s define the rules to adjust the trades when our profit target is reached.

- Specifically, let’s close the call options if the trades make 150% or greater return on investment.

- As you can see from the charts below, the slight modification to the trading rules results in significantly different performance results.

- The OptionStack platform makes it easy to modify and backtest various different trading strategies to maximize your profit.